The ultimate foreign gift tax reporting requirements overview

Wiki Article

Exactly How Coverage Foreign Inheritance to IRS Functions: Trick Insights and Guidelines for Tax Coverage

Maneuvering the intricacies of reporting foreign inheritance to the IRS can be challenging. There specify limits and kinds that people should recognize to guarantee compliance. Inheritances surpassing $100,000 from non-resident aliens need specific interest. Failure to stick to these standards may bring about fines. Recognizing the nuances of tax obligation effects and required documents is important. The adhering to sections will lay out important insights and guidelines for effective tax obligation coverage.Understanding Foreign Inheritance and Its Tax Obligation Implications

When people get an inheritance from abroad, it is essential for them to comprehend the connected tax ramifications. In the USA, acquired properties are generally exempt to earnings tax obligation, yet the estate where the inheritance comes may have particular tax responsibilities. International inheritances can make complex issues, as various nations have differing policies concerning estate tax obligations. People have to know that while they may not owe taxes on the inheritance itself, they may be in charge of reporting the worth of the foreign property to the Irs (INTERNAL REVENUE SERVICE) Furthermore, currency exchange rates and assessment methods can influence the reported well worth of the inheritance. Recognizing these aspects is essential to prevent unanticipated tax obligations. Looking for assistance from a tax specialist experienced in global inheritance legislations can offer quality and assurance conformity with both U.S. and foreign tax needs.

Reporting Demands for Inherited Foreign Assets

The coverage demands for inherited international properties involve details limits and limits that taxpayers must understand. Compliance with IRS regulations demands the appropriate tax return and recognition of potential charges for failure to report. Comprehending these components is essential for individuals getting foreign inheritances to prevent lawful issues.Reporting Thresholds and Limits

While going across the intricacies of acquired international properties, comprehending the reporting limitations and thresholds set by the IRS is crucial for compliance. The IRS requireds that united state taxpayers report international inheritances surpassing $100,000 from non-resident aliens or international estates. This limitation applies to the total worth of the inheritance, encompassing all assets obtained, such as money, actual estate, and investments. Additionally, any kind of foreign economic accounts completing over $10,000 should be reported on the Foreign Checking Account Record (FBAR) Failure to stick to these limits can lead to considerable fines. It is vital for taxpayers to properly examine the worth of acquired international possessions to guarantee timely and certified reporting to the IRSTax Obligation Forms Summary

Charges for Non-Compliance

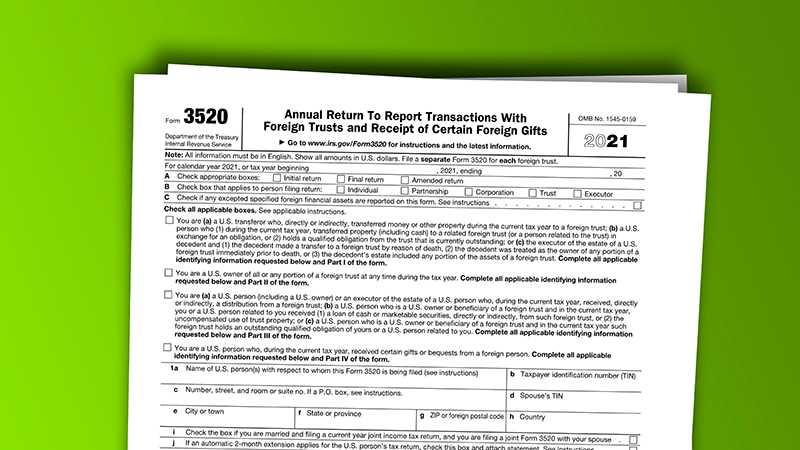

Failing to follow coverage requirements for acquired international assets can lead to significant fines for united state taxpayers. The IRS enforces stringent guidelines pertaining to the disclosure of foreign inheritances, and failures can bring about fines that are frequently significant. Taxpayers may face a charge of up to $10,000 for stopping working to submit Type 3520, which reports foreign gifts and inheritances surpassing $100,000. Additionally, proceeded non-compliance can rise penalties, potentially getting to up to 35% of the worth of the inherited property. Failing to report can additionally cause extra severe effects, including criminal charges for unyielding neglect. Taxpayers must continue to be vigilant to avoid these effects by guaranteeing accurate and prompt coverage of international inheritances.Key Kinds and Documents Needed

When a specific gets an international inheritance, it is necessary to recognize the vital kinds and documents needed for conformity with IRS policies. The key type required is the IRS Kind 3520, which have to be submitted to report the receipt of the international inheritance. This type gives in-depth info regarding the inheritance, including the identity of the international decedent and the value of the acquired properties.In addition, if the inherited property includes foreign savings account or various other financial assets, the person might require to submit the Foreign Financial institution Account Report (FBAR), FinCEN Type 114, if the total value exceeds $10,000. Appropriate documents, such as the will or estate papers from the foreign territory, should also be accumulated to validate the inheritance insurance claim. Maintaining thorough records of all communications and transactions related to the inheritance is essential for accurate reporting and compliance with IRS demands.

Tax Treaties and Their Influence On Inheritance Tax

Recognizing the effects of tax treaties is vital for individuals obtaining international inheritances, as these arrangements can significantly impact the tax commitments connected to acquired properties. penalties for not filing Form 3520. Tax obligation treaties between countries frequently supply certain guidelines on how inheritances are tired, which can result in reduced tax obligation responsibilities or exceptions. A treaty may stipulate that particular types of inheritances are not subject to tax in the recipient's nation, or it may allow for credit histories versus tax obligations paid abroad.

People must acquaint themselves with the certain provisions of appropriate treaties, as they can differ significantly. This understanding aids ensure compliance with tax obligation guidelines while maximizing potential advantages. Furthermore, understanding just how treaties interact with residential laws is vital to accurately report international inheritances to the IRS. Consulting with a tax expert well-versed in global tax legislation might be suggested to browse these complicated policies effectively.

Typical Errors to Prevent When Reporting Inheritance

Numerous individuals think they can quickly browse the intricacies of reporting foreign inheritances, they typically forget vital details that can lead to considerable errors. One usual blunder is falling short to report the inheritance in the correct tax year, which can lead to fines. In addition, some people disregard to convert foreign assets into united state bucks at the ideal exchange price, subsequently misrepresenting their value. An additional frequent oversight involves misunderstanding the reporting thresholds; individuals might think they do not require to report if the inheritance is below a particular amount, which is incorrect. Misclassifying the type of inheritance-- such as dealing with a gift as an inheritance-- can complicate reporting commitments. Lastly, individuals often fail to keep thorough documentation, which is vital for verifying insurance claims and avoiding audits. Understanding of these pitfalls can greatly improve compliance and reduce the danger of monetary effects.Looking For Professional Assistance for Complicated Situations

Maneuvering the complexities of reporting foreign inheritances can be frightening, particularly for those with complicated economic circumstances. People dealing with problems such as numerous foreign assets, varying tax obligation implications throughout territories, or elaborate household characteristics may gain from specialist help. Tax obligation experts focusing on international tax obligation law can give very useful insights into the nuances of IRS laws, making certain conformity while lessening potential obligations.Engaging a qualified public accounting professional (CERTIFIED PUBLIC ACCOUNTANT) or tax attorney with experience in foreign inheritance can help clear up coverage demands, determine applicable exemptions, and strategize best tax strategies. They can aid in finishing essential kinds, such as Form 3520, and taking care of any kind of additional disclosure needs.

Inevitably, looking for professional guidance can alleviate anxiety and improve understanding, enabling individuals to concentrate on the emotional aspects of inheritance as opposed to becoming overwhelmed by tax obligation IRS Form 3520 inheritance complexities. This proactive approach can result in more beneficial outcomes in the lengthy run.

Often Asked Inquiries

Do I Required to Record Foreign Inheritance if I'm Not a united state Resident?

Non-U.S. residents generally do not need to report international inheritances to the IRS unless they have details connections to united state tax legislations. Nonetheless, it's a good idea to seek advice from a tax obligation professional to clarify private situations.Are There Penalties for Failing to Record Foreign Inheritance?

Yes, there are fines for failing to report international inheritance. People might deal with considerable fines, and the IRS can enforce added consequences for non-compliance, possibly affecting future tax obligation filings and monetary standing.Can I Deduct Expenses Connected To Taking Care Of Inherited Foreign Possessions?

Expenditures associated with handling inherited foreign assets are typically not insurance deductible for tax obligation functions. Nonetheless, individuals ought to seek advice from a tax obligation expert for support customized to their certain circumstances and potential exemptions that may use.How Does Foreign Currency Impact the Value of My Inheritance Record?

International currency fluctuations can significantly affect the reported worth of an inheritance. When converting to united state bucks, the exchange rate at the time of inheritance and reporting identifies the last reported value for tax obligation purposes

What Occurs if My Foreign Inheritance Is Held in a Depend on?

It might complicate reporting requirements if an international inheritance is held in a depend on. The trust's framework and tax implications should be assessed, as recipients could deal with differing tax commitments based on jurisdiction and trust fund kind.The Internal revenue service mandates that United state taxpayers report foreign inheritances exceeding $100,000 from non-resident aliens or international estates. In addition, any kind of international monetary accounts amounting to over $10,000 should be reported on the Foreign Financial Institution Account Report (FBAR) People inheriting foreign properties should commonly report these on Type 8938 (Statement of Specified Foreign Financial Properties), if the overall worth exceeds particular thresholds. Depending on the nature of the inheritance, various other kinds such as Form 3520 (Yearly Return To Record Purchases With Foreign Trusts and Invoice of Particular International Presents) might also be necessary. In addition, if the inherited residential or commercial property includes international bank accounts or other financial possessions, the individual may need to file the Foreign Financial institution Account Report (FBAR), FinCEN Kind 114, if the complete worth surpasses $10,000.

Report this wiki page